How Efficiently Does a Company Use What It Owns to Generate Profit?

When you invest in a business, whether it’s a Canadian bank, a global tech company, or an Indian manufacturing firm, the underlying question is always the same:

Is this business using its capital efficiently to generate profit?

Profit numbers alone don’t tell that story — especially when growth, debt, and capital structure vary across industries.

This guide explains four return metrics in a friendly, practical way that helps you judge business quality:

- ROA – Return on Assets

- ROE – Return on Equity

- ROCE – Return on Capital Employed

- ROIC vs WACC – The Ultimate Value Creation Test

Let’s walk through them using clear examples and straightforward logic.

ROA — How Efficiently Does the Company Use Everything It Owns?

ROA — How Efficiently Does the Company Use Everything It Owns?

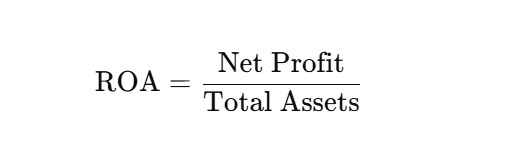

ROA stands for Return on Assets, and it measures how much profit a company earns relative to all the assets it controls.

Formula for ROA

Simple Example

Imagine two companies:

- Company A earns $10 million profit and owns $100 million in assets → ROA = 10%

- Company B also earns $10 million profit but owns $300 million in assets → ROA = 3.3%

Even though both companies have the same profit, Company A uses its assets more efficiently.

Real-World Bank Context — Canada vs India

Canadian Banks

Major Canadian banks tend to generate ROA below 1%, which is typical for large diversified banks with high asset bases.

For example:

- National Bank of Canada’s ROA ≈ 0.75% (as of late 2025) for the most recent quarter — roughly in line with peer norms for the sector. (GuruFocus)

Other Canadian banks like Bank of Montreal have reported ROA around ~0.6–1.0% historically. (www.alphaspread.com)

Indian Banks

In contrast, some Indian private sector banks have historically reported higher ROA figures in certain years:

- HDFC Bank’s ROA has often been in the ~1.6–1.7% range over multi-year averages. (Our Wealth Insights)

Larger public sector banks tend to be lower overall, but many private Indian banks have achieved ROA above 1.5% at times, reflecting different business models and margin structures.

Takeaway:

Banking ROA is much lower than typical corporate ROA because loans and interest income dominate balance sheets. But even within banks, ROA varies by geography and business mix — a nuance this metric captures well.

Why ROA Matters

ROA is especially useful when comparing companies that rely heavily on their asset base to generate profit.

Consider:

- Banks and financial institutions

- Profits come from interest on loans and investments

- A 0.8% ROA may be strong given massive asset sizes

- Asset-heavy manufacturers and infrastructure firms

- Higher ROA signals better utilization of plants, machinery, inventory, etc.

ROA alerts you when assets aren’t pulling their weight.

ROE — How Well Is Shareholder Money Being Compounded?

ROE — How Well Is Shareholder Money Being Compounded?

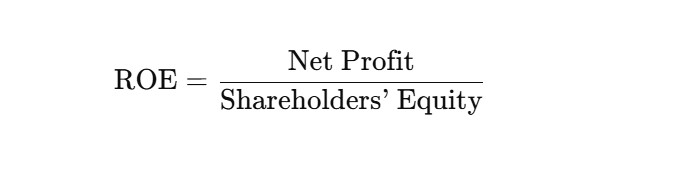

ROE stands for Return on Equity. It shows how much profit the business generates relative to money invested by shareholders.

ROE Formula

A 20% ROE means the company earns $0.20 profit for every $1 of equity.

But unlike ROA, ROE is sensitive to leverage (how much debt a company uses). More debt often shrinks equity and boosts ROE, even if the business itself isn’t operating better.

When ROE Is Most Useful

ROE shines in businesses where debt is a normal, regulated part of the model:

- Banks — equity cushions risk and reflects retained profits

- Insurance companies — capital supports underwriting

- Asset managers — equity funds operations and future earnings

In these sectors, ROE gives insight into shareholder return power, as opposed to just operational efficiency.

ROCE — How Strong Is the Business Engine?

ROCE — How Strong Is the Business Engine?

Now we move to a metric that combines both operating performance and capital strength:

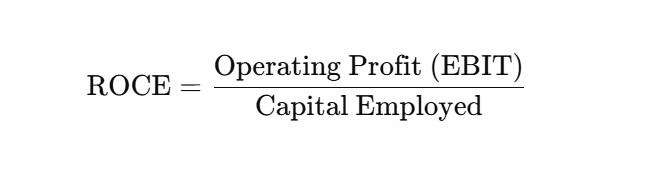

ROCE = Return on Capital Employed

ROCE Formula

Where:

This tells you how well the business generates profits from the capital it needs for long-term operations.

Simple Example

Company X:

- Operating profit (EBIT) = $15 million

- Capital employed = $100 million

→ ROCE = 15%

This means the company earns 15% on the capital that truly matters for operations.

Why ROCE Is Better Than ROE for Many Businesses

In non-financial sectors, ROCE is usually more informative than ROE because it:

- Focuses on operating returns before interest

- Removes distortions introduced by leverage

- Makes businesses comparable regardless of capital structure

ROCE works well in:

- Manufacturing

- Consumer goods

- Chemicals

- Capital goods

- Infrastructure

It shows whether the core business is strong.

How ROA, ROE and ROCE Work Together

How ROA, ROE and ROCE Work Together

Here’s how to use these metrics in sequence:

ROA (Asset Efficiency)

ROA (Asset Efficiency)

Does the business get decent profit from its assets?

If ROA is weak, profits may be superficial.

ROE vs ROCE (Leverage Lens)

ROE vs ROCE (Leverage Lens)

Once ROA looks acceptable:

- If ROE ≈ ROCE, equity returns are rooted in business performance

- If ROE > ROCE, leverage is boosting returns — check risk

- If ROE < ROCE, equity returns are weak relative to business strength

This comparison reveals hidden leverage effects that single metrics miss.

The Ultimate Test: ROIC vs WACC (Real Value Creation)

The Ultimate Test: ROIC vs WACC (Real Value Creation)

Finally, we reach the most important metric in your toolkit:

- ROIC (Return on Invested Capital) — measures the return business earns on all capital invested in operations

- WACC (Weighted Average Cost of Capital) — represents the minimum return required by investors (both equity and debt)

The Value Creation Rule

If:

→ The company is creating economic value.

If:

→ The company is not earning enough to justify capital invested.

Why This Matters Most

Profit growth and shiny margins don’t matter if the business can’t earn more than its cost of capital.

This is the economic benchmark for long-term investing.

Sector Guide (Reader-Friendly)

- Banks & Financials

- Focus on ROA and ROE (banks operate large asset books and use regulated leverage)

- Asset-Heavy Corporations

- Start with ROA, then check ROCE to assess operating efficiency

- Core Operating Businesses

- ROCE reveals engine strength

- ROE shows shareholder returns

- Compounders & Capital Allocators

- ROIC vs WACC tells you whether this business truly creates value

Final Takeaway (Simple and Practical)

Think of returns like lenses:

- ROA shows whether assets are being used well

- ROE shows how shareholder money is compounded

- ROCE shows the business engine’s strength

- ROIC vs WACC shows whether the business earns real economic value

Used together — especially in the context of your Canadian and Indian market insights — they give you a clear, holistic picture of business quality.